Global payment processors

Stripe

Stripe has become one of the world's leading payment platforms, and for good reason. It offers an impressive blend of developer-friendly tools and business features that make it a top choice for e-commerce businesses of all sizes.

What sets Stripe apart is its flexibility and global reach. The platform handles payments in more than 135 currencies and offers local payment methods across dozens of countries. For businesses with international ambitions, this makes Stripe particularly attractive.

Setting up Stripe is straightforward, especially if you have some technical resources. Their documentation is among the best in the industry, making implementation relatively painless even for complex setups. For non-technical users, many e-commerce platforms offer pre-built Stripe integrations that require minimal setup.

Stripe's pricing structure is transparent—typically 2.9% + $0.30 per transaction in the US, with similar rates adjusted for other regions. While not the cheapest option for high-volume merchants, the extensive feature set often justifies the cost.

One significant advantage of Stripe is its robust fraud prevention system. Their machine learning tools automatically detect and block suspicious transactions, potentially saving you from costly chargebacks. For businesses in high-risk categories, this alone can make Stripe worth considering.

The main drawback? Stripe doesn't have the consumer brand recognition of PayPal or Klarna, so it doesn't serve as a trust signal to customers in the same way. It's primarily a backend payment processor rather than a consumer-facing brand.

Shopify payments

For B2C e-commerce businesses using Shopify, Shopify Payments stands out as our top recommendation in most scenarios.

What makes Shopify Payments so attractive is how easy it is to set up combined with its affordability. Store owners don't face setup fees or transaction costs beyond the standard rates. There's also a sliding scale of pricing—the more advanced your Shopify plan, the lower your payment processing rates.

This pricing structure means even small online stores can access affordable payment processing. As your business grows and you upgrade your Shopify plan, your payment costs actually become more favorable.

The obvious drawback is that Shopify Payments only works if you're using Shopify as your e-commerce platform. While Shopify is excellent, if you're already established on a different platform, you'll need to look elsewhere.

The key advantages include:

- Pricing that scales with your business (2% for Basic, 1% for Shopify and 0.5% for Advanced)

- Works well in Sweden and internationally

- Includes Klarna integration, giving Swedish merchants the ability to offer split payments and buy-now-pay-later options

You can always add other payment services to your Shopify store alongside Shopify Payments, letting customers choose what works best for them.

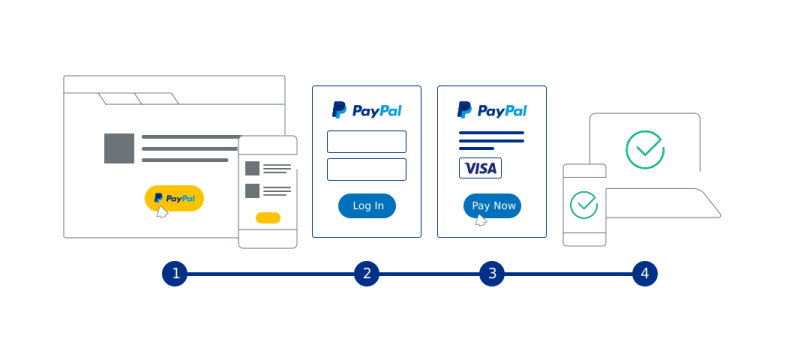

PayPal

While PayPal dominates globally as one of the world's best-known payment services, it hasn't gained the same traction among Swedish online retailers. This likely stems from Sweden's strong local alternatives specifically built for the Swedish market. Swedish shoppers are accustomed to options like Swish and split payment solutions from Klarna, Payson, and others.

For international sales, however, PayPal remains an excellent choice.

Getting started with PayPal is straightforward with no setup costs for their checkout system.

If you're not registered in Sweden but want to sell to Swedish customers, PayPal offers an advantage: you won't need a redemption agreement to sell in the Swedish market.

PayPal lets you start accepting payments with minimal red tape. By contrast, many Swedish payment solutions can take around two weeks to get up and running.

One common myth worth dispelling: PayPal isn't just for customers with PayPal accounts. Your customers can make card payments through PayPal without creating an account.

Nordic payment solutions

The Nordic markets (Sweden, Denmark, Norway, Finland) have developed some of the world's most advanced payment ecosystems, with unique solutions that dominate local e-commerce:

Swish

Swish stands out as one of the most recognized payment methods in Sweden. Unlike the other services we're covering, you can't connect your online store directly to Swish. Instead, you need to go through either a bank or a payment provider that has Swish integration.

This is because Swish was created as a collaboration between Swedish banks. The typical process involves contacting your bank to set up a Swish agreement, for which they'll charge a fee. Once that's in place, you can add Swish as a payment option in your checkout—assuming your checkout system supports it.

For example, WooCommerce users can install a plugin that enables Swish payments.

The cost of Swish varies depending on your bank. Nordea's business customers currently pay SEK 50 monthly, while Sparbanken charges SEK 900 yearly (about SEK 75 per month).

Swedbank has a different approach, charging SEK 1.5 per transaction for business customers on their Basic and Plus packages. Other business customers pay SEK 2 per transaction.

(Note that these prices can change and should be treated as estimates. The actual costs might vary based on your relationship with your bank and the business package you're using.)

Klarna

Klarna has become one of Sweden's payment success stories and enjoys strong brand recognition among Swedish consumers. Using Klarna at checkout instead of less-known payment options typically boosts conversion rates noticeably.

Our team has first-hand experience with Klarna. One downside we've encountered is the time it takes to configure settings properly. Their support can be slow, and we've run into limitations that might make alternatives more attractive in some cases.

Companies focused on dropshipping face particular challenges, as Klarna requires specific agreements. If you're selling B2B across different markets, you should know that Klarna only supports B2B payments for Swedish customers.

Another consideration is cost - Klarna isn't among the cheaper options. Pricing starts at 3.50 SEK per transaction plus 2.79% of the transaction value.

Despite these drawbacks, Klarna's brand power in Sweden is undeniable. They offer a well-rounded solution that lets customers choose between immediate card payment or split payments.

For sellers, a key advantage is getting paid immediately, regardless of whether your customer chooses to pay Klarna all at once or over time.

If Klarna's direct integration seems too complex or expensive, consider using a payment service that includes Klarna alongside other payment options. Many services let you offer Swish and other payment methods alongside Klarna.

In short, Klarna works well for e-commerce companies targeting Swedish consumers, but its complexity and cost mean simpler alternatives might be preferable for some businesses.

Svea Checkout

Svea Ekonomi has established itself as a major player in the Swedish market, with a payment solution aimed primarily at established online businesses. Choosing Svea as your main payment provider brings several advantages.

Svea Checkout works for both B2B and B2C sales environments. As a Svea Ekonomi customer, you'll get a personal contact who can help solve issues specific to your business model.

The service offers extensive customization options and integrates with many popular e-commerce platforms in Sweden. For businesses interested in offering split payments, Svea Ekonomi can provide generous terms regarding interest rates.

Billmate

Billmate provides another solid payment option with a good balance of features and pricing. It's part of the Invoice group, which also includes Invoice Inkasso and Invoice Finance.

Beyond its own payment methods (including installments, invoicing, and standard card payments), Billmate Checkout also incorporates third-party payment solutions like Swish and direct bank payments.

Be aware that these additional payment services require separate agreements before you can offer them at checkout.

For example, direct bank payments require an agreement with Trustly Group. Once you're set up to accept direct payments (where customers log into their bank account to complete the transaction—something many consider more secure), you'll pay an agreed fee to Trustly. Billmate adds its own "Gateway fee" of 0.5% on the transaction value.

BankID authorization and authentication

When targeting Northern European markets, particularly Sweden, incorporating BankID can dramatically improve both security and conversion rates. BankID has become Sweden's standard for digital identity verification, used by nearly all major banks, government agencies, and businesses.

For your customers, BankID offers a familiar and trusted way to identify themselves and sign digital agreements quickly and securely—whether on your website, in your app, or even over the phone. Because it's widely used across websites and mobile services, customers already know how to use it and trust the process.

Our experience implementing BankID for clients has shown that a properly executed BankID integration can increase conversion rates by up to 35% while significantly reducing fraud attempts.

To offer BankID in your services, you'll need:

- A relaying party certificate (RP certificate) that gives you access to the BankID system

- Technical preparation of your site to handle login and signing with BankID

- Compliance with BankID's implementation guidelines and best practices

The process requires specific technical expertise, but the business benefits make it worthwhile for companies serious about the Swedish market. Our team specializes in guiding businesses through the entire implementation process, from obtaining certificates to final technical integration.

Other important regional payment solutions

Beyond the Nordic region, several other important regional payment methods are worth considering depending on your target markets:

- In Germany, many consumers prefer direct bank transfers through solutions like Sofort and Giropay

- The Netherlands has strong adoption of iDEAL for online payments

- China's market is dominated by Alipay and WeChat Pay

- Latin America sees heavy use of local payment methods like Boleto in Brazil and OXXO in Mexico

For businesses serious about succeeding in specific regional markets, incorporating these local payment methods is often essential for maximizing conversion rates.